Thinking of donating to a university or another nonprofit but want income as well as tax advantages from the gift? A Charitable Gift Annuity or CGA is worth exploring, especially as we head into 2025. The reason: the relatively high payout levels on CGAs have been extended into 2025.

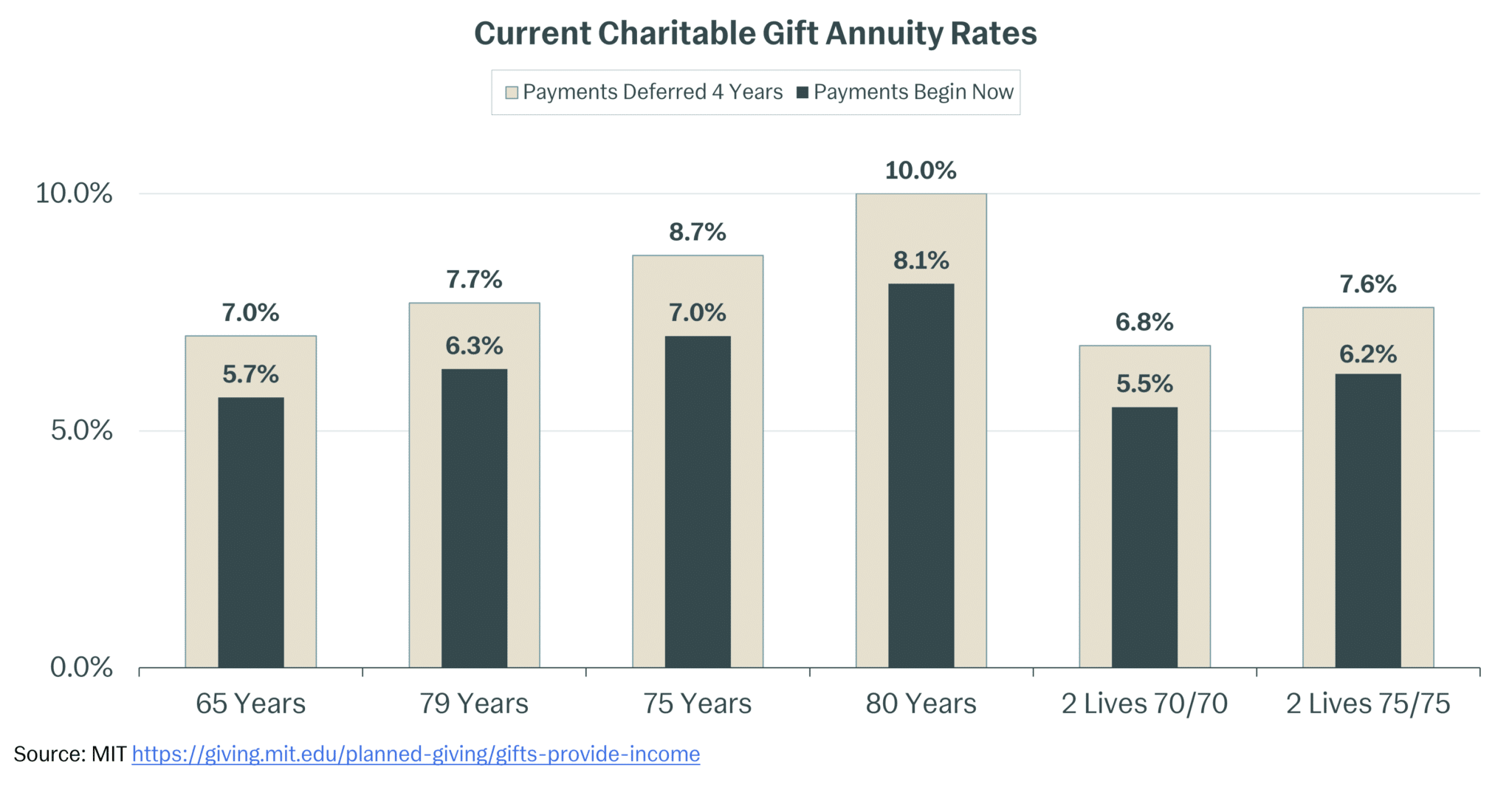

CGA payout levels are based on interest rates set by the American Council on Gift Annuities (the ACGA) and can be found here and illustrated in the chart below based on the age of the donor at the time of the gift. The CGA payout rates have climbed steadily since 2022 as the Federal Reserve increased its key interest rate from near zero to a peak of 5.25% – 5.5%. Even though the Federal Reserved then lowered its key rate three times in 2024, the ACGA has announced it will not change its rates until further notice.

Here is their rationale for keeping their rates steady: “While many observers may focus on the Fed’s headlined grabbing moves, ACGA’s proven processes take a view moderated by attention to actual rates over a multi-month time frame. ACGA will continue to monitor Fed activity, bond yields, and other economic and market factors as it considers the appropriateness of its current rate guidance.” As noted in LNW’s January 2025 Flash Report, the Federal Reserve’s actions have had a mixed impact on U.S. rates: U.S. short-term interest rates are down but longer-term rates have held steady or increased.

How a CGA Works

Thousands of U.S. nonprofits offer CGAs and they are quite common among major colleges and universities. A CGA is a simple contract between you and a nonprofit, let’s say your alma mater. You agree to make a donation of cash, appreciated financial assets and in some cases this can include real estate or life insurance policies. Your donation is set aside in a reserve account and invested. Based on your age at the time of donation, you receive a fixed payment (monthly, quarterly or annually) for the rest of your life or for the lives of both you and your spouse. After you pass away, the university keeps what is left in the annuity to fund general or specific needs you have specified.

In addition to income, you may also be eligible to take a tax deduction at the time of the original gift, based on the estimated amount that will eventually go to the university after all the annuity payments have been made. A portion of the payments made to you may also be tax-free for a period of time based on your life expectancy.

MIT Example: At MIT, the starting age for CGAs is 50, the minimum donation is $20,000, and the payouts can be deferred for four years after donation. MIT’s planning giving website provides a calculator you can type into to see results for various scenarios: https://giving.mit.edu/planned-giving/calculator

Let’s assume 67-year-old Sarah donates $500,000 in appreciated stock to MIT via an CGA on January 16, 2025. Using the MIT online calculator, here is what Sarah can expect if the cost basis for her stock (what she originally paid) was $250,000:

2024 tax deduction: $176,125.

Fixed annual payment: $29,500 for the remainder of Sarah’s life.

Until Sarah reaches age 85, to be taxed as follows:

$8,850 would be tax-free

$8,850 taxed as capital gains (20% max at current rates)

$11,800 taxed as ordinary income at her highest marginal rate

After age 85, the entire $29,500 would be taxed as income to Sarah.

Donations from IRAs, 401(ks): Starting in 2024, IRA owners aged 70 ½ and older can opt to donate in any one year up to $54,000 (indexed for inflation) of their qualified charitable distributions (QCDs) to one or more CGAs. This is allowed for only one tax year and there are certain requirements. There are several limitations in making this kind of gift, but certain donors may find it satisfies their financial and philanthropic needs and should discuss it with their financial and tax advisors.

What Else to Consider

Supporting higher education and being able to specify in many cases what your funds will be used to fund, plus the various tax breaks make CGAs attractive. However, you should also be clear-eyed about the limitations of CGAs:

- You will lose access permanently to the donated funds (this is an irrevocable gift)

- The payout is fixed – it will be adjusted to reflect inflation — and it is likely to be a bit lower than what you can get from a regular annuity

- Part of your payment will be taxed as income and if you outlive your life expectancy, all of it will be taxed as income

- Payments may be lower than with a non-charitable annuity because the primary purpose is for nonprofit support

- Cannot be used to support multiple charities unless you set up multiple annuities

- Financial stability of the institution; there have been very few defaults on CGAs over the past 100 years but as with any annuity, the solvency of the issuer is a factor.